What Indian Exporters Must Know About UK Payment Terms?

Before you sell in the UK, it’s essential to understand how payments and due diligence work. Here’s the quick breakdown.

Before you start exporting to the UK, it’s important to understand how payment terms typically work and how to protect yourself from risk. Most UK buyers prefer credit-based arrangements, such as Net 30, 60, or 90 days, which means you’ll often receive payment weeks after your goods are delivered. While this helps you stay competitive, it can also create cash flow gaps if you’re unprepared.

You can have brilliant products, perfect pricing, and strong demand, but none of it matters if you run out of money waiting for payments.

In this section, we’ll cover how UK payment terms typically work and outline simple due diligence steps that every founder should take before closing a deal.

Understanding UK Payment Culture

Before we dive into solutions, let’s understand the problem.

British businesses operate on credit. It’s baked into their business models. Large retailers, especially, have optimised their cash flow by extending payment terms as far as possible.

Typical Payment Terms by Buyer Type for B2B Businesses:

Small independent retailers: 30% advance or Net 30

Medium retailers/boutiques: Net 30-45

Large retailers (John Lewis, Next, etc.): Net 60-90

Supermarkets (for food/FMCG): Net 90-120

Online marketplaces (NOTHS, etc.): Net 30-45

Distributors: Net 45-60

However, if you’re selling direct-to-consumer (Shopify, Amazon, your website), you get paid immediately:

Shopify: 2-3 days after sale

Amazon: 14 days after sale

PayPal/Stripe: 2-7 days after sale

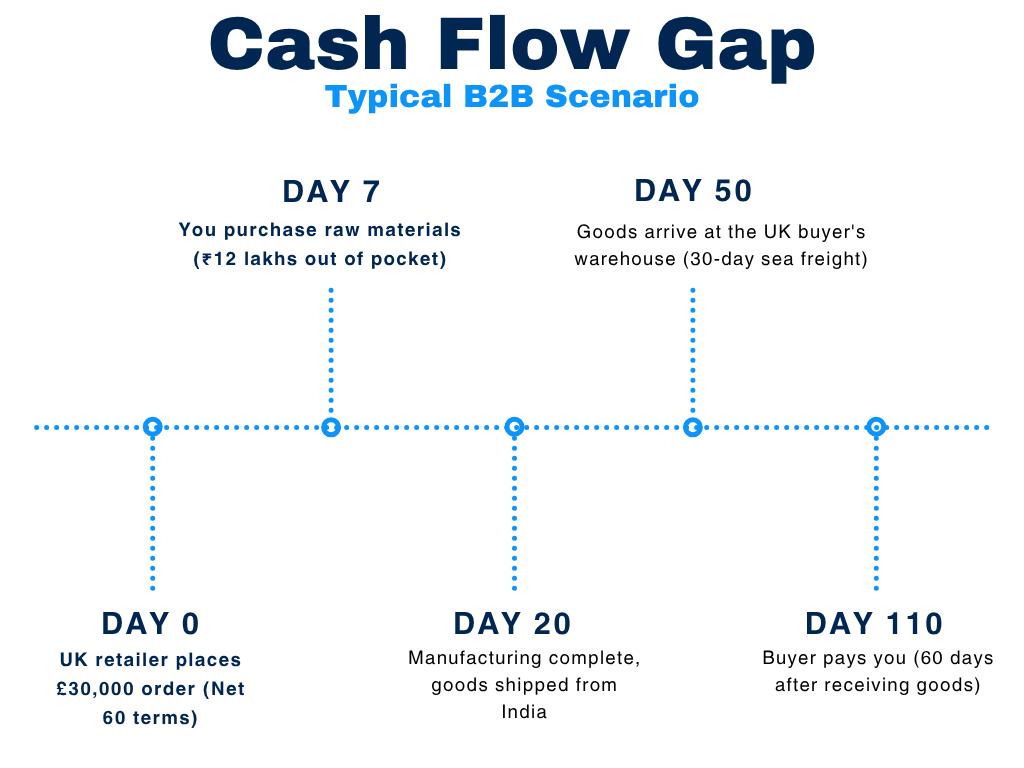

This is why D2C, despite smaller order sizes, often has better cash flow than B2B. How? Let’s walk through a typical B2B scenario:

You’ll be out of pocket for 110 days. And that’s assuming everything goes perfectly- no delays, disputes, or “the payment got stuck in processing.”

During those 110 days, you still need to:

Pay your suppliers

Cover salaries

Fund your next production run

Manage your own operating expenses

This is the point where most exporters struggle, and many break.

Payment Terms for the UK Market

Not all payment terms are equal. Here’s how to negotiate terms that protect your cash flow, especially when you’re new to the UK market.

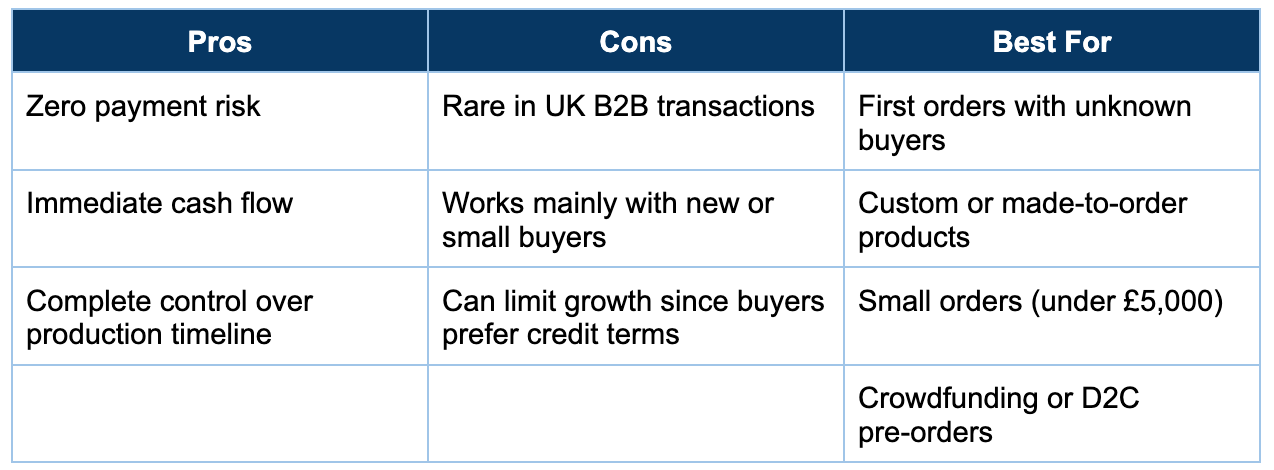

1. Advance Payment (100% Upfront)

In this method, the buyer pays the entire amount before you begin manufacturing or shipping. It’s the safest option for exporters since there’s no payment risk and you get instant cash flow, allowing you to control production timelines fully. However, it’s uncommon in the UK B2B trade- buyers usually prefer credit terms.

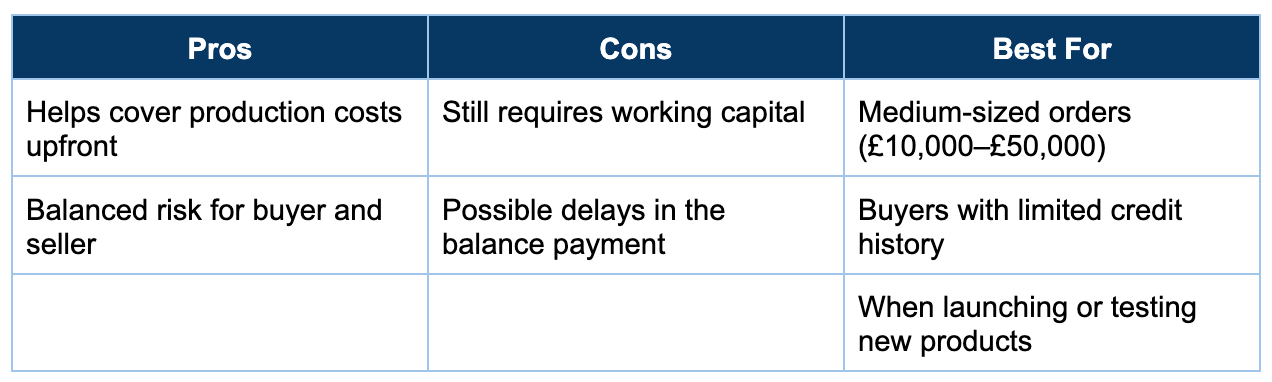

2. Partial Advance + Balance Against Documents

In this payment structure, the buyer pays a portion of the total amount upfront, typically 30–50%, and the remaining balance is cleared before or upon the release of shipping documents, such as the Bill of Lading. This model helps cover your production costs while maintaining a fair balance of risk between both parties.

It’s a typical arrangement for early transactions with new UK buyers or when selling mid-sized orders.

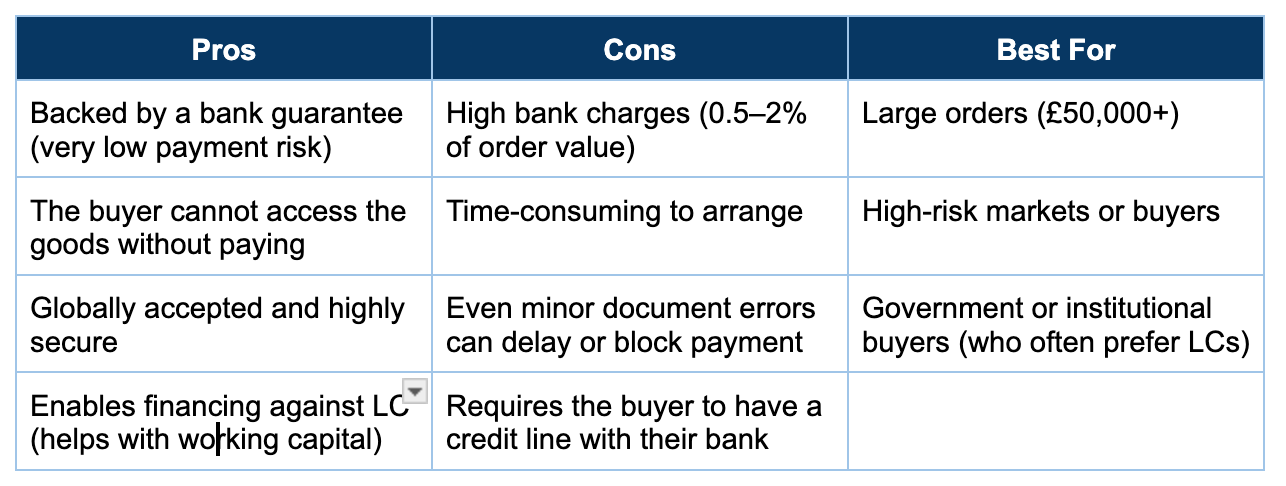

3. Letter of Credit (LC)

A Letter of Credit is a payment mechanism in which the buyer’s bank guarantees payment upon receipt of the required shipping documents. It’s one of the most secure methods in international trade, minimising payment risk for exporters.

The process involves coordination between the buyer’s and seller’s banks to ensure that payment is only released when all terms and documents match the LC conditions.

Types:

Sight LC: Payment is made immediately upon document submission.

Usance LC: Payment is made after 30/60/90 days- offering credit terms but with a bank guarantee.

Cost Breakdown Example:

£50,000 order

LC charges: 1.5% = £750

Swift/communication charges: £50-100

Document processing: £100-200

Total: £900-1,050 (usually split between buyer and seller, or negotiated)

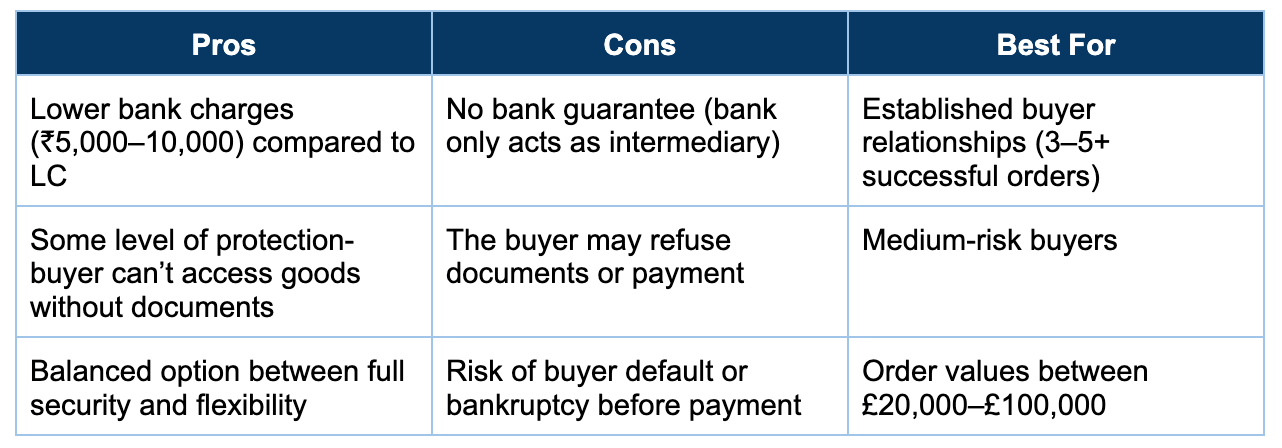

4. Documentary Collection (CAD/DP - Cash Against Documents)

In a Documentary Collection, you ship the goods and send the shipping documents through your bank to the buyer’s bank. The buyer’s bank releases these documents only when the buyer makes a payment or accepts a promise to pay at a later time.

It’s a cost-effective alternative to a Letter of Credit, offering moderate security while keeping banking costs lower.

Types:

D/P (Documents against Payment): Buyer pays immediately before receiving the documents.

D/A (Documents against Acceptance): Buyer accepts a bill of exchange (a formal promise to pay later) and receives the documents upfront.

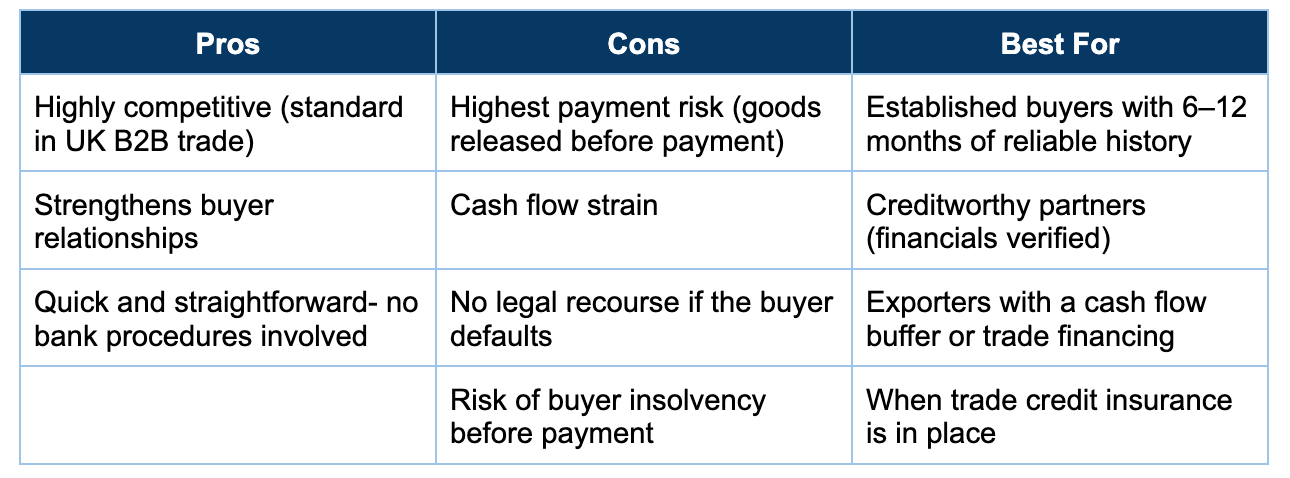

5. Open Account / Credit Terms (Net 30/60/90)

Under an Open Account arrangement, you ship the goods first, and the buyer pays later- typically 30, 60, or 90 days after receiving the invoice. This is the most buyer-friendly and commonly preferred payment method in the UK, especially for long-term relationships.

While it helps build trust and drive repeat business, it also carries the highest risk for exporters since payment is entirely dependent on the buyer’s integrity and financial stability.

Risk Mitigation:

Start with Net 30, gradually extend to Net 60/90 as trust builds

Set credit limits per buyer (e.g., max £50,000 outstanding)

Use trade credit insurance (more below)

Get personal guarantees from directors (for smaller companies)

Due Diligence

Before you extend credit terms to any UK buyer, do your homework.

Basic Checks (Free/Cheap)

1. Companies House Check

Before working with a new UK buyer, always verify their background on Companies House, the official UK government register of businesses. It provides key details like company registration status, directors, financial filings, and annual accounts.

The service is either free or costs up to £3 per report.

What to Look For?

Late filings: may indicate poor financial discipline

Frequent director changes: potential instability or ownership issues

Low net worth or high liabilities: signs of financial weakness

Recent incorporation: limited track record, proceed cautiously

2. Google Search

Search company name + “reviews,” “complaints,” “payment issues”

Check their social media presence

See if they’re actively trading (website updated, social posts recent)

3. LinkedIn Research

Use LinkedIn to verify the legitimacy and credibility of a potential buyer. A company’s LinkedIn presence often reveals more than just surface-level details- you can assess its size, team stability, and overall authenticity.

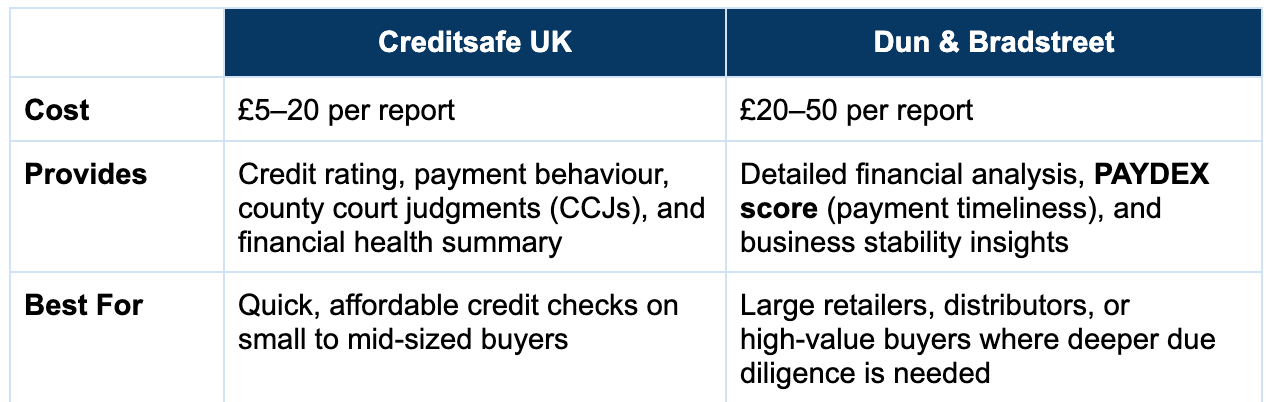

Paid Credit Checks

For high-value or long-term deals, it’s worth investing in a professional credit report to assess a buyer’s financial reliability. Services like Creditsafe UK and Dun & Bradstreet provide detailed insights into a company’s credit score, payment history, and overall economic health.

When to Pay for Credit Reports?

Orders over £25,000

New buyers asking for Net 60+ terms

Any red flags from free checks

Buyer is a relatively new company (<3 years)

Rule of Thumb: If you’re uncomfortable risking the order value, pay for a credit report. £20 is nothing compared to losing £30,000.

Cash Flow Survival: Practical Tips

While you’re building financing and risk systems, here are tactical ways to survive cash flow crunches:

Negotiate Better Terms with Suppliers: If UK buyers want Net 60, ask your Indian suppliers for Net 45. This will reduce your cash gap.

Offer Discounts for Early Payment: “2/10 Net 60” = 2% discount if paid within 10 days, full payment due in 60 days. Many UK buyers will take this.

Batch Production Smartly: Don’t manufacture until you have multiple orders. Reduces working capital needs.

Use Wise/Payoneer for Forex: Save 2-3% on every transaction vs traditional banks. Over £500,000, that’s £10,000-15,000 saved.

Build a Cash Reserve: Once profitable, keep 3-6 months of operating expenses in reserve. This cushion is priceless.

Mix D2C and B2B: D2C pays faster. Use D2C cash flow to fund B2B working capital needs.

Final Thoughts

For most founders, the most challenging part of growing internationally isn’t finding buyers- it’s managing the cash flow gap between shipping goods and getting paid. You’re covering production costs, paying suppliers, and running operations long before the money hits your account. And when UK buyers prefer credit terms like Net 30 or Net 60, that gap can feel even wider.

That’s why it’s important to start smart. When dealing with new buyers, begin with safer payment terms like partial advances or Letters of Credit, and only move to open account terms once trust is built.

Always do your homework- check your buyer’s background, financials, and track record before shipping. These simple steps can save you from sleepless nights and give you the confidence to grow sustainably.

In the next part, we’ll dive deeper into the financing options available to help you manage cash flow, take on bigger orders, and scale confidently in the UK market without feeling the cash crunch.

Dive into Vault today & unlock a world of possibilities.