Trade Credit Insurance: A Simple Breakdown for Indian Exporters

In this article, we’ll break down Trade Credit Insurance in simple terms- what it is, how it works, why it matters for Indian exporters, and how it can help you scale globally.

If you’re an Indian founder exporting to countries like the US, UK, Canada or UAE- remember this: the biggest risk is not finding customers. The biggest risk is getting paid on time once you’ve already shipped goods or delivered services abroad.

On the surface, everything may look perfectly safe- great brand, known retailer, “big order”, strong demand. But if the buyer delays, defaults or becomes insolvent internationally, it becomes a nightmare. Global legal recovery is slow, expensive and incredibly draining for a young company. And banks aren’t comfortable financing foreign receivables without security, so they either reduce your limit or straight up refuse financing for those invoices.

This is where Trade Credit Insurance comes in. It protects your export invoices if the buyer overseas fails to pay.

In this blog

We break down how Trade Credit Insurance works, the typical cost structure, how payouts work, country-specific considerations for Indian exporters (US, UK, UAE, Canada), and a comparison table across major Indian insurers - so you know who to shortlist before applying.

How Does Trade Credit Insurance Work?

Trade Credit Insurance is actually pretty simple in practice. Here’s how it plays out inside your export cycle:

1. Insurer checks your buyers first

Before providing coverage, the insurer evaluates the creditworthiness of each buyer you sell to and assigns a credit limit for each. This is the maximum exposure they’re willing to insure.

2. You take a policy on those receivables

You can insure a select few high-risk buyers or your entire export receivables portfolio, depending on the level of diversification and predictability in your book.

3. You continue doing business like normal

You ship, you invoice, you operate. Nothing really changes operationally in your sales cycle.

4. If a buyer doesn’t pay

In the event that the buyer defaults due to insolvency, goes bankrupt, or exceeds the defined delay (for example, remains unpaid even after 180 days), you are eligible to file a claim.

5. Insurance pays a significant portion back to you

The insurer reimburses the majority of the unpaid amount, usually around 80–90% of the invoice value.

Trade Credit Insurance solves for three critical realities of modern Indian exporters:

Cash Flow Volatility

Buyer Concentration Risk

Financing Needs

Let’s say ABC Textiles Pvt. Ltd., an Indian exporter, sells ₹50 lakh worth of fabric to a UK buyer with 60-day payment terms. Due to the buyer’s bankruptcy, the payment never arrives.

With trade credit insurance covering 90% of losses, ABC Textiles recovers ₹45 lakh from the insurer- preserving cash flow and stability.

Types of Trade Credit Insurance

Trade credit insurance can be customised based on business needs. Common types include:

1. Whole Turnover Policy

Covers all domestic and/or export receivables. Ideal for businesses with multiple clients and continuous sales.

2. Key Account Policy

Covers only major customers or a few high-value buyers whose default could significantly impact the business.

3. Single Buyer Policy

Provides protection against non-payment by one specific customer. Common in businesses with concentrated buyer exposure.

4. Export Credit Insurance

Protects exporters against non-payment due to both commercial risks (such as buyer insolvency) and political risks (including war, sanctions, or currency inconvertibility).

Who Should Opt for Trade Credit Insurance?

Trade credit insurance is beneficial for:

Exporters trading with foreign clients or in volatile markets.

Manufacturers and wholesalers selling goods on credit.

SMEs that rely on a few large clients for most of their revenue.

Businesses expanding into new markets where buyer credibility is uncertain.

Companies managing long credit cycles or tight working capital positions.

If you’re doing ₹5–10 crore+ in annual exports, it’s time to evaluate Trade Credit Insurance seriously, and if just 1–2 buyers make up over 40% of your revenue, you should get it immediately because buyer concentration is a silent time bomb.

To put it in perspective,

TCI premium: ~0.3% on a ₹10 crore export book = ~₹3 lakh/year

One buyer defaults on a ₹50 lakh invoice

With coverage, your recovery could be ₹45 lakh

So, technically, it pays for itself the first time something goes wrong.

What’s Not Covered in Trade Credit Insurance?

While comprehensive, trade credit insurance typically does not cover:

Disputes over product quality or contract terms

Fraudulent transactions

Currency fluctuations

Delayed payments (unless classified as default)

Sales to related parties (e.g., subsidiaries or group companies)

Trade Credit Insurance in India

In India, trade credit insurance has evolved significantly over the past few years.

Until 2021, ECGC was the dominant provider of export credit insurance in India, particularly for political risk.

In 2021, IRDAI (Insurance Regulatory and Development Authority of India) liberalised trade credit insurance. This allowed private general insurers to offer TCI products to a broader range of businesses, including MSMEs, SaaS exporters, and D2C brands for commercial risks.

This policy shift enabled Indian founders to access world-class trade credit products, often in partnership with global insurers such as Allianz Trade, Coface, or Atradius.

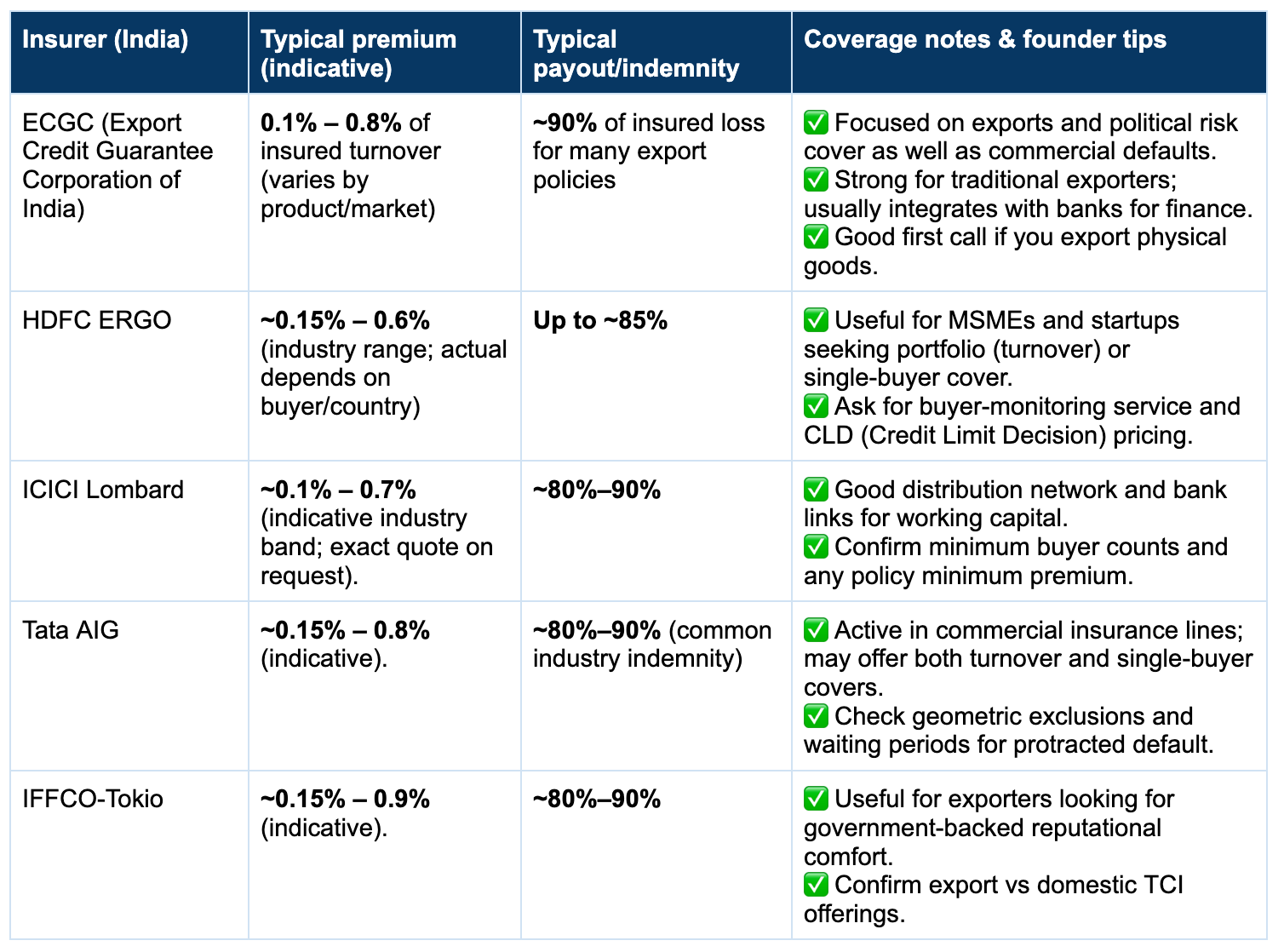

Major Indian Providers:

ECGC: Export credit & political risk cover for traditional exporters.

HDFC ERGO, ICICI Lombard, Tata AIG, IFFCO Tokio: Private sector policies for both domestic and international trade.

Note: Premium rates are indicative and may vary based on factors such as buyer risk, industry, coverage structure, and past claims history. Always request a customised quote.

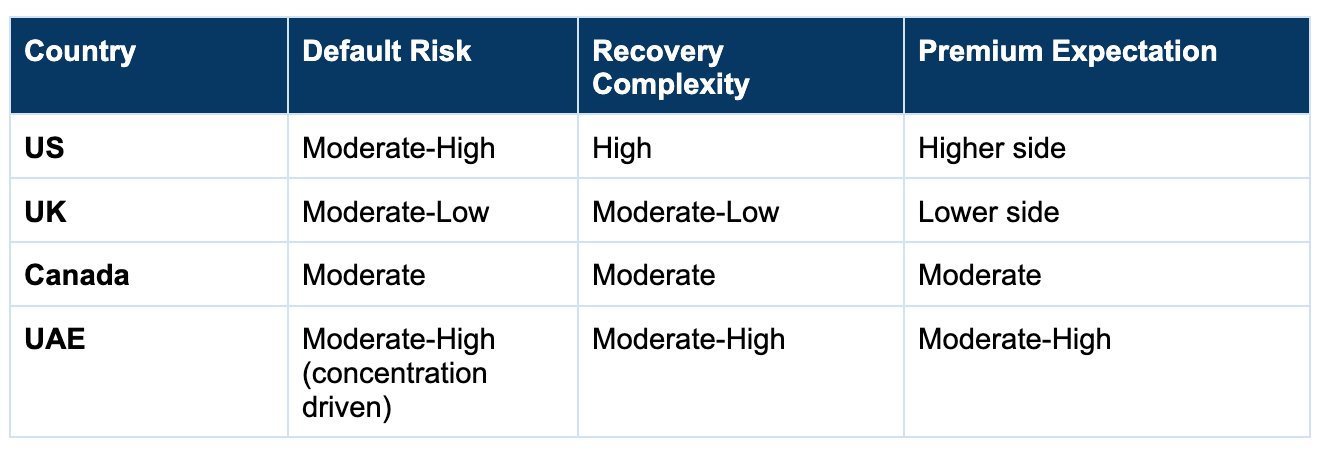

Country-specific considerations for Indian exporters (US, UK, Canada, UAE)

When exporting, the buyer's country matters significantly because credit risk, enforcement, collection costs, and legal friction differ substantially by region. The way you choose insurer structure, limits, and premium tolerance should shift based on the destination market.

1. United States

The US legal system is strong, but recovery is extremely expensive + slow.

Defaults typically happen due to supply chain cash cycles or inventory build-up risks on the buyer side.

Premium is usually slightly higher for the US, and limit setting is stricter.

Ask your insurer for:

Protracted default coverage for US buyers

Higher indemnity %

Credit limit per specific retailer chain (not generic group cover)

2. United Kingdom

The UK is relatively predictable, with lower credit friction vs the US.

Insolvency filings are formalised and transparent, so recovery predictability is strong.

Ask your insurer for:

Multi-buyer turnover cover (works well for the UK)

Better premium rate bargaining (UK risk generally ranks favourably)

Short waiting period (possible leverage argument)

3. Canada

Similar buyer behaviour patterns to those in the US, but with lower volatility.

Manufacturing and wholesale distributors are stable, but energy and commodities swings hit Canada’s receivables badly.

Ask your insurer for:

Sector-specific underwriting (very important for Canada)

Check if they have Canadian credit bureau tie-ups or data partnerships

4. UAE

Robust Indian trade corridor, but buyer concentration risk is exceptionally high- many exporters depend on just 3–5 UAE buyers.

Premiums may be slightly higher than in the UK/Canada but usually lower than in the US.

Ask your insurer for:

Single buyer cover top-up

Frequent buyer re-underwriting

Clarity on fraud-risk exclusions

Quick mental model for founders exporting from India:

How to Choose the Right Policy?

Here’s what to consider before buying trade credit insurance:

Coverage Scope: Domestic, export, or both.

Customer Concentration: If you rely heavily on a few buyers, opt for key account or single-buyer coverage.

Credit Limits: Ensure your insurer’s buyer limits align with your invoice volumes.

Claims Process: Understand documentation and timelines for claim settlement.

Premium Costs: Premiums typically range between 0.1% and 1% of annual turnover, depending on sector risk and coverage extent.

Final Thoughts

Trade Credit Insurance is one of those quiet compounding unlocks that almost no one talks about, but every serious exporter uses once they scale past ₹5-10 crore annual export volume.

It reduces downside risk, increases bank leverage, improves working capital efficiency, and allows you to take bolder geographic bets without fear.

If you’re planning to scale exports to the US / UK / Canada / UAE over the next 12 months, it’s high time for you to give Trade Credit Insurance some thought because one unpaid invoice shouldn’t kill your global expansion.

Dive into Vault today & unlock a world of possibilities.