How to Finance the UK Expansion of Your Business?

Whether you're a D2C brand, a services company, or a B2B exporter, understanding your financing options early helps you plan confidently and avoid cash-flow surprises.

Expanding your business to the UK is a significant milestone- it means your product has the potential to compete on a global stage. But for most founders, the cash flow gets stretched thin. You’re paying suppliers, managing production, covering logistics, and running your team- all while waiting weeks or even months to get paid by buyers overseas.

In this article, we’ll discuss the different ways you can finance your UK expansion, from advance payments and letters of credit to export financing options that keep your business moving even when payments are delayed.

1. Traditional Bank Lending: Export Credit / Working Capital Loans

Traditional bank loans remain one of the most common ways to finance exports and manage cash flow during international expansion. Your bank provides a loan or overdraft facility to help fund production, raw material purchases, and other export-related expenses.

These facilities are typically short-term and secured against collateral, such as property or other business assets. Depending on your business stage and export cycle, banks usually offer three types of facilities.

Packing Credit: Short-term loan to buy raw materials and manufacture goods for confirmed export orders.

Post-Shipment Credit: Bridge loan covering the gap between shipment and buyer payment.

Working Capital Overdraft: Flexible facility to manage operational cash flow and recurring expenses.

This route works best for established businesses with at least 3 years of financial history, large confirmed export orders, and a willingness to provide collateral.

Typical Terms

Interest Rate: 8–12% per annum (India)

Tenure: 90–180 days

Collateral: Often requires property, asset mortgage, or personal guarantee

Processing Fee: 0.5–1% of the loan amount

Loan Amount: Typically 70–80% of order or LC value (based on your financials and collateral)

How to Apply?

To apply, you’ll need to do the following:

Approach your existing bank with export order details.

Submit documents like Export order/LC, company financials, IT returns, collateral documents, etc.

The bank evaluates eligibility and approves a credit limit, which you can draw from as needed for each shipment.

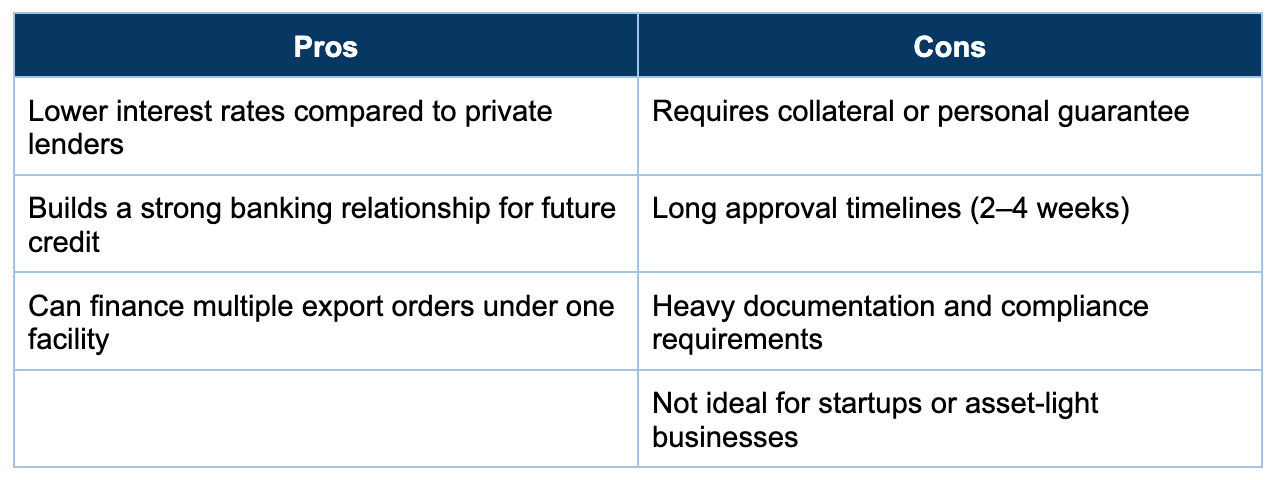

Pros & Cons

2. Trade Finance (Letter of Credit Financing)

Trade finance through Letter of Credit (LC) financing helps exporters unlock working capital without waiting for the buyer’s payment.

When your buyer opens an LC, your bank can advance you the payment (at a slight discount) against it, giving you quick access to funds while the bank collects payment from the buyer’s bank once the LC matures.

There are two main types of LC financing.

LC Discounting/Negotiation: Bank pays you immediately (minus discount) before LC maturity

Pre-shipment finance against LC: A Loan to manufacture goods based on the LC received

This method is ideal when you need immediate liquidity, and your buyer agrees to use an LC. It’s beneficial for large orders (£30,000+), first-time or high-risk buyers, or situations where you need cash right after shipment.

Typical Terms

Discount rate: 1-3% of LC value (depending on LC tenor)

No collateral needed (LC itself is security)

Payment within 3-5 days of document submission

Example:

If you receive a £50,000 LC (60-day usance), you ship goods and submit documents.

The bank pays you £49,000 immediately (after 2% discount).

The bank collects £50,000 from the buyer’s bank after 60 days.

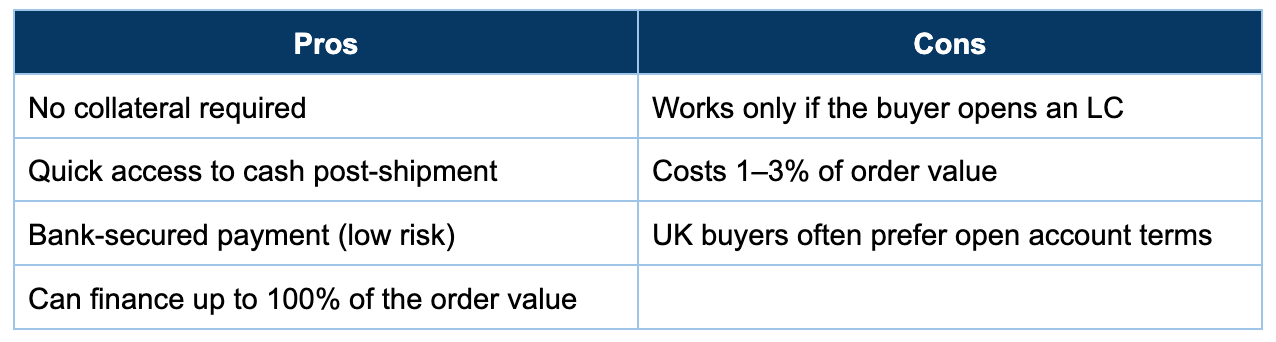

Pros & Cons

3. Invoice Financing / Factoring

Invoice financing (or factoring) is a practical way to unlock cash tied up in unpaid invoices- mainly when your UK buyers operate on long credit terms. Instead of waiting 30, 60, or 90 days for payment, a finance company buys your invoice at a slight discount and gives you most of the money upfront.

When the buyer eventually pays, the finance company settles the remaining balance after deducting fees.

There are two main types of invoice financing.

Invoice Factoring (Disclosed):

In invoice factoring (disclosed), the finance company buys your invoice outright and collects payment directly from your buyer, meaning the buyer knows a third party is involved. You typically get 80–90% of the invoice value upfront, and the remaining 10–20% once the buyer pays (after fees).

Invoice Discounting (Non-Disclosed):

In invoice discounting (non-disclosed), on the other hand, you still collect the payment yourself, while the finance company advances you money against your invoice- the buyer doesn’t know about this arrangement.

In India, providers like Drip Capital, KredX, M1xchange, and Indiabulls Commercial Credit offer export-focused invoice financing solutions.

This model works best for exporters dealing with multiple UK buyers on credit terms, with annual export turnover above £500,000, and for founders who need ongoing working capital but lack sufficient collateral for traditional bank loans.

Typical Terms

Advance rate: 80-90% of the invoice value immediately

Fee: 1-3% of invoice value

Interest: 1-2% per month on outstanding amount

Example:

If you ship goods worth £50,000 to a UK retailer on Net 60 terms:

The factor advances £42,500 immediately (85%).

They charge a £1,000 fee (2%).

When the buyer pays after 60 days, you receive the remaining £6,500.

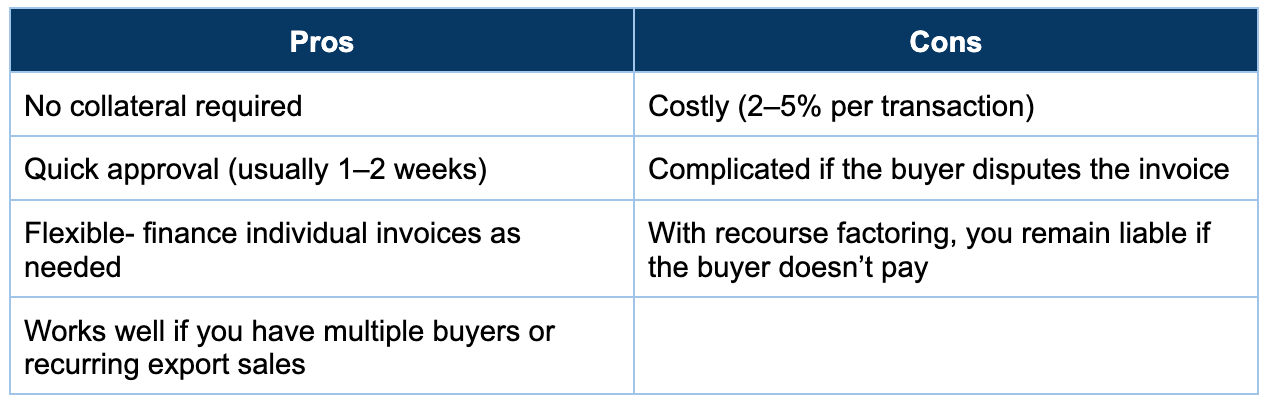

Pros & Cons

4. Revenue-Based Financing (For D2C Brands)

Revenue-based financing (RBF) is a modern, flexible funding option designed especially for D2C and e-commerce brands. Instead of pledging collateral or giving up equity, you get funding based on your current and projected revenue- usually your online sales data.

Repayments are made as a fixed percentage of your daily or weekly revenue, meaning you pay more when sales are high and less when they slow down.

Global providers like Shopify Capital, Clearco, and Uncapped accept Indian businesses with proven traction, while Indian players like GetVantage, Klub, and Velocity serve domestic brands with UK demand.

It works best for D2C brands doing £30,000+ in monthly revenue, needing quick, collateral-free funds to restock or scale.

Typical Terms

Advance: 1-6 months of monthly revenue (e.g., if you do £50,000/month, get £50,000-300,000)

Repayment: 8-20% of daily sales until principal + fee repaid

Fee: 6-12% flat fee on the amount borrowed

No fixed tenure (depends on your sales velocity)

Example: You borrow £100,000 at a 10% fee, meaning your total repayment is £110,000. If you agree to repay 15% of your daily sales, and your average daily revenue is £3,000, you’ll pay £450 per day, completing repayment in roughly 8 months.

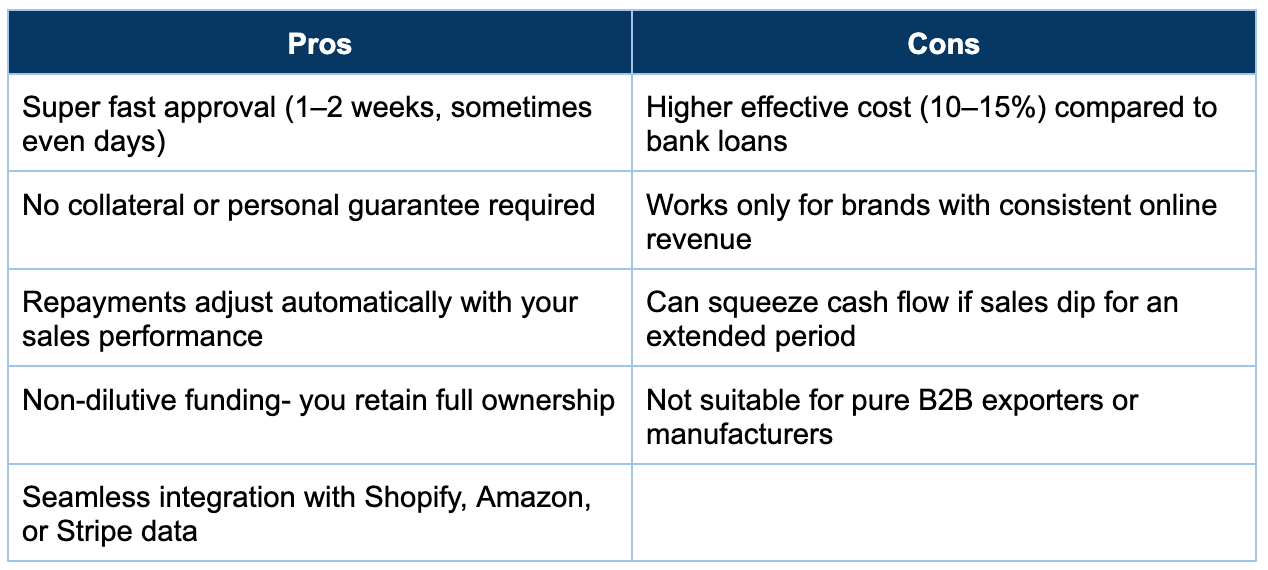

Pros & Cons

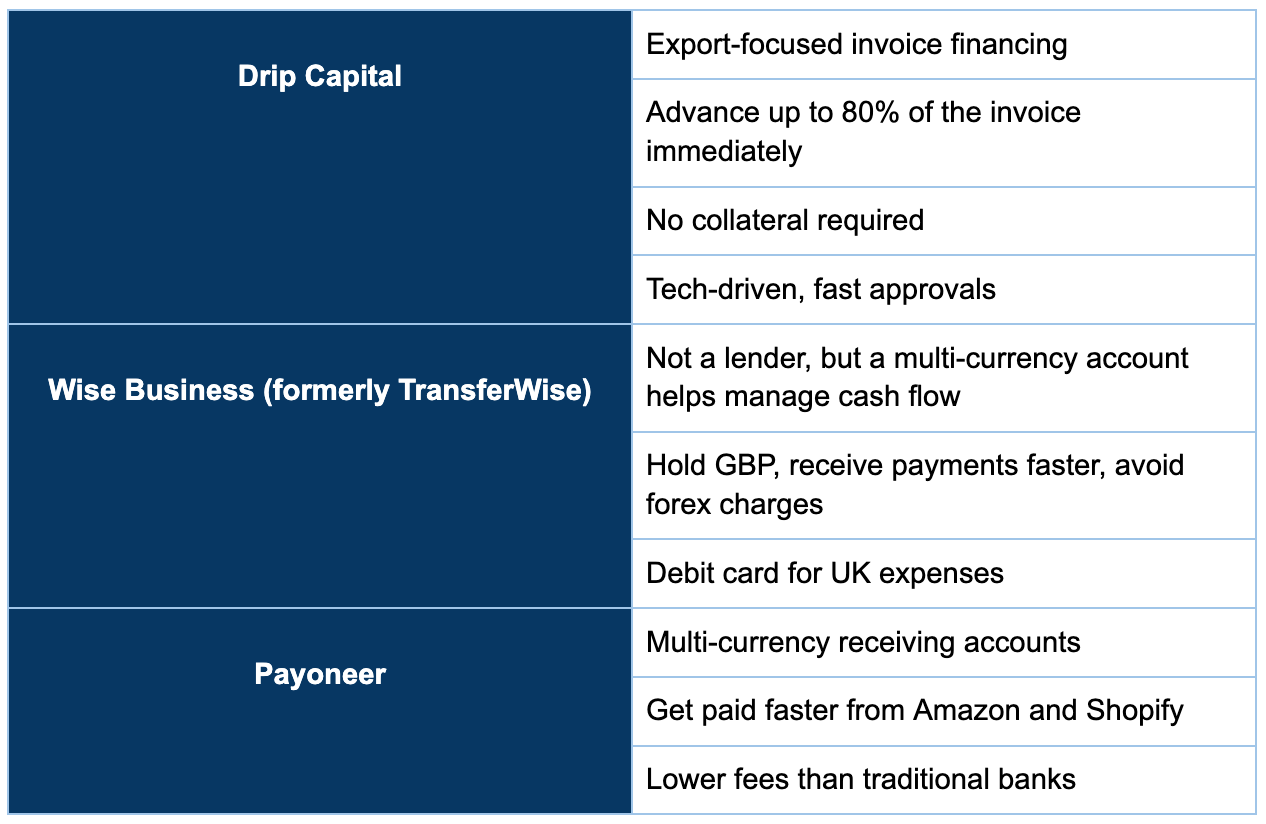

5. Equity-Free Dilution: Alternative Funding

Not every founder wants to give up equity or deal with long approval cycles of traditional banks. That’s where platform-based funding comes in, designed to give exporters quick, flexible access to capital and seamless ways to manage international payments.

These options are beneficial for Indian businesses expanding into the UK, as they simplify cash flow, reduce forex friction, and speed up cross-border transactions.

6. Government Schemes & Subsidies

For Indian exporters, the government offers several schemes designed to make international expansion more affordable and less risky. Some key programs are:

ECGC Export Finance: A government-backed initiative that provides export credit insurance and financing at lower rates than commercial lenders. It protects you from political and commercial risks, such as buyer insolvency or payment delays, and allows banks to lend more confidently to exporters.

Interest Equalisation Scheme (IES): Under this program, the government subsidises 3–5% of the interest rate on export credit for eligible MSMEs. This means your effective borrowing cost drops significantly, improving profitability and competitiveness.

You can access both ECGC and IES benefits through your existing relationship bank. When applying for export credit or packing finance, ask specifically about ECGC coverage and IES eligibility.

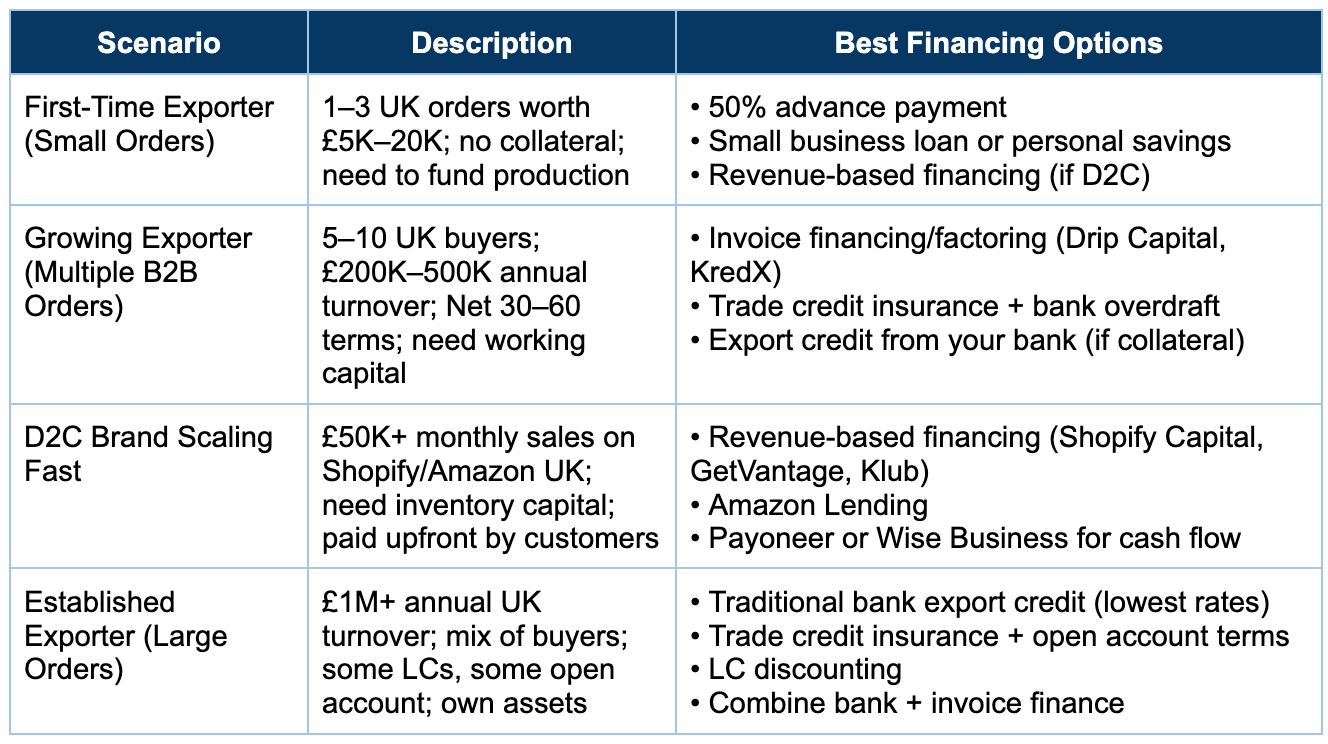

How to Choose the Right Financing for Your Business?

Every founder faces that moment- you’ve got the orders, the demand looks strong, but your cash flow says otherwise. The big question becomes: how do you fund growth without running out of oxygen?

The right financing depends on where your business is today- your cash flow cycle, the type of buyers you work with, and how much risk you’re comfortable taking. Here’s a quick guide:

Final Thoughts

Financial security may not sound exciting. It won’t make for viral Instagram posts or flashy founder stories, but it’s the quiet difference between businesses that scale steadily and those that collapse under their own growth. You can have the perfect product, pricing, and logistics, but none of it matters if you run out of cash.

In the beginning, play it safe- ask for partial advance payments, set strict credit limits, and use trade credit insurance. Once you’ve built trust and figured out which buyers are dependable, you can ease up, offer better terms, and scale faster.

Dive into Vault today & unlock a world of possibilities.