How to Calculate Your Startup’s Valuation?

Startup valuation doesn’t have to be complex. This guide breaks down the most common valuation methods, what investors actually look for, and how founders can arrive at a realistic number.

Startup valuation is one of the most confusing yet important topics for founders. Ask five people how to value a startup, and you’ll get five different answers. That’s because valuation is not a fixed formula; it’s a mix of numbers, narrative, and negotiation.

This article breaks down:

What startup valuation really means

The most commonly used valuation methods (with examples)

How valuation changes by stage

What Is Startup Valuation?

Startup valuation is the estimated economic value of your company at a given point in time. It determines:

How much equity do you give up in a fundraise

Your ownership dilution

Investor expectations and future fundraising dynamics

There are two key terms you must understand:

1. Pre-money Valuation

The value of your startup before a new investment comes in.

2. Post-money Valuation

The value of your startup after the investment.

Key Factors That Impact Your Valuation

Startup valuation is influenced by far more than just revenue or user numbers. Investors evaluate a combination of quantitative metrics and qualitative signals to assess both the size of the opportunity and the risk involved in capturing it.

Market Size (TAM): Big markets justify big outcomes.

Traction: Revenue, users, growth rate, retention.

Team: Founder-market fit matters more than resumes.

Business Model: Predictable revenue > one-time sales.

Growth Rate: Fast-growing startups command premium valuations.

Timing & Market Sentiment: Bull markets inflate valuations; bear markets compress them.

Valuation Methods Used for Startups

Unlike mature businesses, startups can’t be valued using a single formula or past financial performance. Most are still early, fast-evolving, and optimising for growth over profits. As a result, startup valuation relies on a combination of market benchmarks, future potential, and investor return expectations.

Different methods are used depending on the startup’s stage, traction, and business model- often with multiple approaches used together to arrive at a reasonable valuation range rather than a fixed number.

1. Comparable Company Analysis (Market-Based Valuation)

Comparable Company Analysis values a startup by benchmarking it against similar companies that have recently raised capital or exited in the same sector, stage, and geography. Instead of starting from internal projections, this method looks outward- at what the market is already paying for startups with comparable business models, traction levels, and growth profiles.

Metrics such as ARR, revenue, GMV, or active users are paired with commonly observed multiples (for example, revenue or ARR multiples) to arrive at an estimated valuation.

For more mature or profitable businesses, CCA may also rely on traditional financial multiples such as EV/EBITDA, EV/EBIT, or Price-to-Earnings (P/E). These are typically relevant when cash flows are stable and profitability is predictable, and are therefore more common in later-stage or pre-IPO valuations rather than early-stage startup fundraising.

Example:

If similar SaaS startups are valued at: 8× ARR

And your startup has: ₹1.5 Cr ARR

Then your estimated valuation: ₹1.5 Cr × 8 = ₹12 Cr

2. Scorecard Valuation Method (Popular for Pre-Revenue Startups)

The Scorecard Valuation Method is commonly used for pre-revenue and early-revenue startups, where financial metrics alone are insufficient to determine value.

Instead of relying on projections, this approach starts with the average valuation of similar-stage startups in the same ecosystem and adjusts it based on how the startup compares across key qualitative factors such as the founding team, market size, product readiness, early traction, and competitive advantage.

Example:

If the average pre-seed valuation in your ecosystem is ₹6 Cr and your startup scores above average on most parameters, investors may bump it up to ₹7–8 Cr.

3. Berkus Method (Idea & MVP Stage)

The Berkus Method is explicitly designed for idea-stage and MVP-stage startups that have little to no revenue and limited historical data. Instead of focusing on financial projections, this method assigns value based on the startup’s ability to reduce key early-stage risks.

A fixed value is attributed to core factors such as a sound business idea, a working prototype or MVP, the quality of the founding team, early strategic relationships, and evidence of initial traction or go-to-market readiness. Each factor typically adds a fixed amount.

Example:

If your startup scores well on 4 out of 5 areas at ₹1.5 Cr each:

Valuation = ₹6 Cr

4. Discounted Cash Flow (DCF) Method

The Discounted Cash Flow (DCF) method estimates a startup’s valuation by projecting its future cash flows and discounting them back to their present value using a rate that reflects risk and time.

In theory, this approach links valuation directly to the startup’s long-term ability to generate cash. In practice, however, DCF is less commonly used for early-stage startups because future cash flows are highly uncertain and small changes in assumptions- such as growth rate, margins, or discount rate- can dramatically alter the outcome.

As a result, DCF is more relevant for later-stage or growth-stage startups with predictable revenue and clearer paths to profitability, and is often used as a supporting reference rather than a primary valuation method.

5. Venture Capital (VC) Method (Exit Scenario Analysis)

The Venture Capital (VC) Method values a startup by working backwards from a future exit outcome rather than current performance. Investors first estimate the startup’s potential exit value- typically through an acquisition or IPO- over a 5–7 year horizon, and then apply a target return multiple (often 10× to 25×) based on the risk involved.

This expected return is used to calculate the startup’s acceptable post-money valuation today, which then determines the pre-money valuation based on the investment amount. Because it aligns valuation directly with investor return expectations, the VC Method is widely used in seed to Series A rounds.

Example:

If a VC expects:

Exit value: ₹1,000 Cr

Desired return: 20×

Then: Post-money valuation today = ₹1,000 Cr ÷ 20 = ₹50 Cr

If they invest ₹10 Cr:

Pre-money valuation = ₹40 Cr

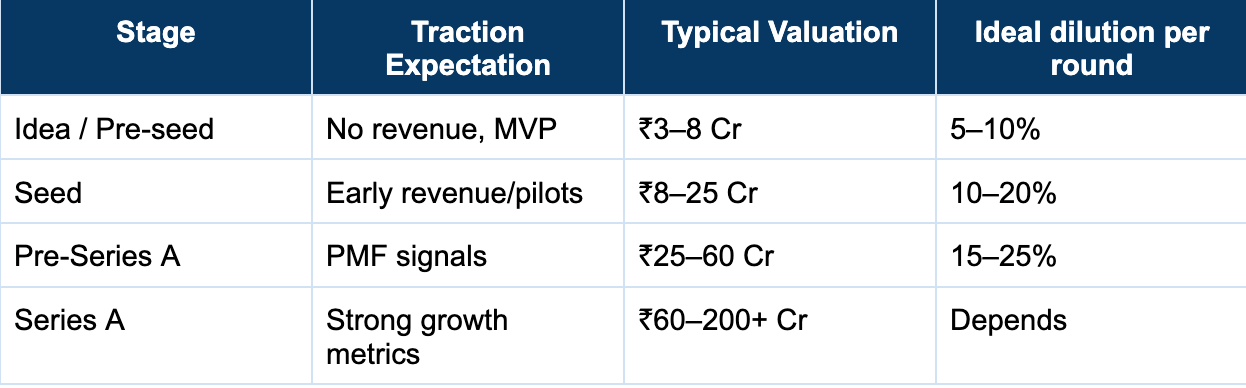

Core Valuation & Dilution Benchmarks (India-focused)

Typical Pre-Money Valuation Ranges:

These ranges reflect recent Indian ecosystem norms across SaaS, fintech, consumer tech, and B2B startups. Hot sectors or exceptional traction can break these ranges.

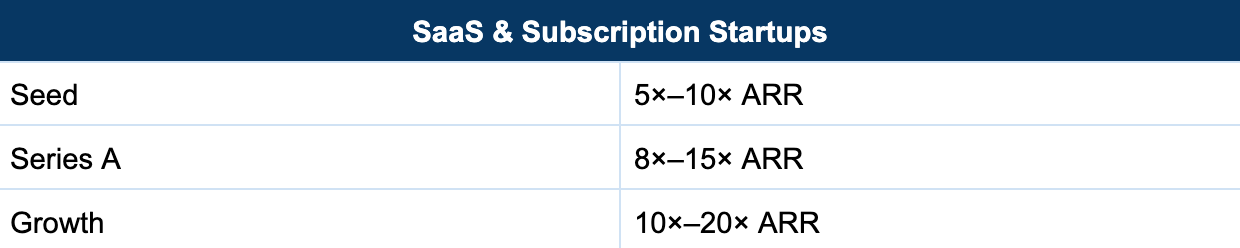

Revenue Multiples as Benchmarks

Revenue multiples are one of the most commonly used benchmarks in startup valuation, especially for companies that have begun generating consistent revenue.

Instead of valuing a startup on profits, investors apply a multiple to key revenue metrics such as ARR, MRR, or annual revenue, based on what comparable companies in the market are trading or raising at. These multiples vary widely depending on the startup’s stage, growth rate, margins, retention, sector, and broader market sentiment.

Example:

A SaaS startup with ₹3 Cr ARR growing at 120% YoY:

Valuation = ₹3 Cr × 10–12 = ₹30–36 Cr

Example:

₹50 Cr GMV

10% take rate → ₹5 Cr revenue

Valuation is often anchored closer to revenue, not GMV

A Founder’s Checklist Before Finalising Valuation

A “good” valuation is not the highest number you can negotiate- it’s the one that gives your startup enough capital, time, and credibility to win the next phase of growth.

The valuation should allow the startup to raise enough capital to secure 18–24 months of runway.

The valuation must be supported by a realistic path to 3–5× growth in key metrics before the next round.

The current valuation should leave clear upside for the next investor.

The valuation should be anchored in current market benchmarks and recent comparable deals.

If the answer to any of these is “no,” the valuation may optimise for short-term validation rather than long-term momentum, and that’s usually a signal to rethink the number before going to market.

Final Thoughts

For most founders, valuation is one of the first moments where the excitement of building meets the reality of fundraising. It’s tempting to chase the highest possible number, but a valuation only works if the business can grow into it.

The proper valuation gives you enough capital to focus on the business, enough runway to learn and iterate, and enough headroom for future investors to get excited. It reflects where your startup is today, while leaving space for where it can realistically go next.

That said, it’s essential to acknowledge the reality: valuation is not decided by formulas alone. In practice, it emerges from the negotiating power of founders and investors. Market benchmarks, scorecards, and models help establish a baseline, but the final number is shaped by demand, momentum, timing, and conviction on both sides of the table. More often than not, valuation is the outcome of a conversation.

At Razorpay Rize, we get it- building a startup is tough. That’s why we’re more than just a space for connecting with other founders. We’ve got programs, tools, and services designed to take some of the weight off the shoulders and make the journey just a little bit easier.

Curious about how we support startup founders?

Dive into Vault today & unlock a world of possibilities.